China’s export restrictions on heavy rare earth elements remain in effect more than a year after they were imposed, according to trade data and industry reports, despite diplomatic efforts to reach a resolution.

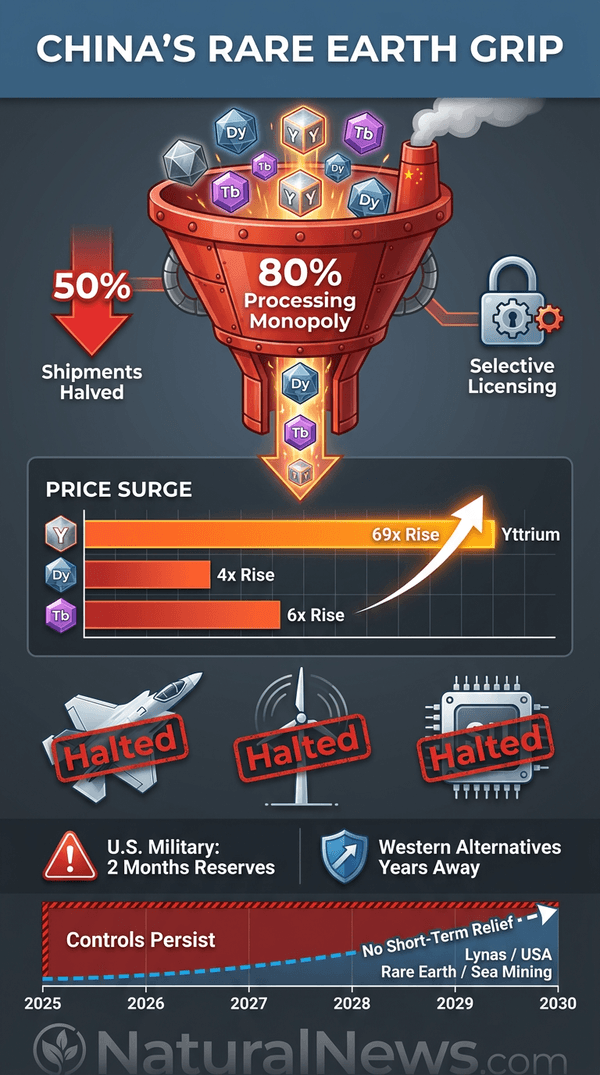

Shipments of key materials including yttrium, dysprosium and terbium have declined by roughly half compared to pre-control levels, data from customs agencies show. The controls, announced in April 2025 as retaliation for U.S. tariffs, have not been lifted, and Beijing has shown no indication of rolling them back.

Background of the Restrictions

The restrictions target a group of heavy rare earths that are essential for advanced defense systems, aerospace components, electric vehicle motors and wind turbines. China's Ministry of Commerce has stated that export applications are being reviewed and approved for eligible buyers.

However, analysts say selective licensing allows Beijing to maintain leverage over strategically sensitive supply chains. China controls about 80% of global rare earth processing, according to industry estimates. [1]

The move, announced in April 2025, was described by Chinese officials as retaliation for U.S. President Donald Trump's tariff hikes. The action covers seven critical rare earth elements vital for defense and technology sectors. [2] The U.S. Department of War has assessed that Washington's reliance on Chinese rare earth processing represents a national security risk, a view echoed by authors who note that the U.S. military depends on rare earths for navigation systems, guidance systems, radios and computers. [3]

Divergence From White House Statements

The persistence of the controls contradicts expectations set during earlier diplomatic engagements. Following a summit in late 2024, the White House indicated that China had agreed to effectively eliminate its export restrictions on rare earths.

A senior U.S. official confirmed in May 2026 that a rare earths deal between the two countries remains in effect, but acknowledged that an extension would be announced at an appropriate time. [4] However, the April 2025 controls were imposed shortly after that summit and remain in force, with no evidence of removal in customs records.

U.S. officials, speaking on condition of anonymity, have confirmed ongoing shortages affecting American manufacturers. The disconnect between diplomatic statements and on-the-ground data has frustrated industry executives.

Analysts cited by Reuters say the selective enforcement allows China to comply with the letter of agreements while preserving its strategic chokehold on supply chains. The U.S. military may have as little as two months of rare earth inventories remaining, according to intelligence and industry sources cited in a March 2026 report. [5]

Global Supply Disruptions and Price Surges

Prices for key rare earths have surged dramatically since the controls took effect. The cost of yttrium increased 69-fold within a year, according to a February 2026 report, halting some aerospace production lines. [6] Price data from commodity pricing agencies shows that dysprosium and terbium have risen four to five times their pre-control levels, while yttrium has increased more than 140 times, according to Argus Media.

Aerospace firms have paused production due to yttrium shortages, and the U.S. government intervened to secure supplies for a major industrial group, officials said. In a 2022 interview, defense industry expert David Dubyne stated that "military F-35 fighter jets have been put on hold because they can't get a key rare earth element from China for their magnets." [7]

The restrictions have also disrupted semiconductor manufacturing, with chipmakers facing dangerous shortages of scandium, threatening 5G technology development. [6] Japan received only a fraction of its previous dysprosium imports, and Germany received no shipments at all, according to customs data from those countries.

Diversification Efforts and Outlook

In response, the United States, Japan Germany and other G7 nations are accelerating efforts to develop alternative mining, refining and magnet production capacity. Australia's Lynas Rare Earths has begun producing heavy rare earths at its Malaysian plant, breaking China's monopoly on the rarest elements. [8] USA Rare Earth announced a $2.8 billion acquisition of Brazil’s Serra Verde Group to expand Western supply chains. [9]

Japan and the U.S. have forged an alliance to mine underwater rare earth deposits near Minamitorishima Island, containing an estimated 16 million tons of rare earth oxides. [10] The U.S. has also signed four major trade agreements with Malaysia, Cambodia, Thailand and Vietnam at the Association of South East Asian Nations summit to secure critical mineral supplies. [11]

But analysts say meaningful alternatives remain years away. U.S. Treasury Secretary Bessent described China’s export curbs as a “real mistake” that triggered a rapid Western shift toward domestic production and alternative suppliers. [12] The long-term solutions are underway, but near-term supply constraints are expected to persist, with some industry experts warning that the situation will deteriorate before improvements materialize.

The U.S. Export-Import Bank's proposed $12 billion project to stockpile critical minerals would initially source supplies from China itself, highlighting the difficulty of decoupling. [13] Robert Bryce, author of "Power Hungry," wrote that "the availability of rare earths is not just about balance of trade; it's also about national security," underscoring the stakes of the ongoing dependency. [3]

Conclusion

The continuation of export controls underscores the deep dependency of Western economies on Chinese rare earth supplies. While new projects are in development, the immediate outlook for manufacturers remains constrained.

The situation highlights the strategic vulnerability of supply chains that took decades to concentrate in a single country. As the U.S. and its allies pursue diversification, the effectiveness of these efforts will determine whether the current supply crisis becomes a permanent structural weakness.

References

- Willow Tohi. "Trumps rare earths push A bid to break Chinas stranglehold but challenges remain." NaturalNews.com. April 27, 2025.

- NaturalNews.com. "Chinas rare earth move threatens US military and tech dominance." NaturalNews.com. April 17, 2025.

- Robert Bryce. "Power Hungry The Myths of Green Energy and the Real Fuels of the Future."

- NaturalNews.com. "Rare Earths Reprieve: US-China Deal Holds as Summit Nears, Exposing Deeper Dependency." NaturalNews.com. May 13, 2026.

- Lance D Johnson. "Pentagon may only have two month supply of rare earths left making US military vulnerable to Chinese controls." NaturalNews.com. March 12, 2026.

- NaturalNews.com. "US defense and tech sectors face crippling shortages of key minerals controlled by China." NaturalNews.com. February 28, 2026.

- Mike Adams. "Mike Adams interview with David Dubyne - September 8 2022."

- ZeroHedge. "China Loses Monopoly Over The Rarest Of Rare Earths." ZeroHedge. April 29, 2026.

- ZeroHedge. "'Critical Inflection Point' Reached As USA Rare Earth Expands With $2.8 Billion Serra Verde Buyout." ZeroHedge. April 20, 2026.

- Ramon Tomey. "Japan and US forge rare earth alliance to break Chinas stranglehold on critical minerals." NaturalNews.com. November 08, 2025.

- Belle Carter. "US secures rare earths and trade deals in Southeast Asia amid China supply concerns." NaturalNews.com. October 28, 2025.

- Ramon Tomey. "Treasury Secretary Bessent Chinas rare earth export curbs a real mistake." NaturalNews.com. November 03, 2025.

- ZeroHedge. "Trump's 'Project Vault' Plans To Initially Buy Rare Earths From China." ZeroHedge. May 5, 2026.

Explainer Infographic

Please contact us for more information.