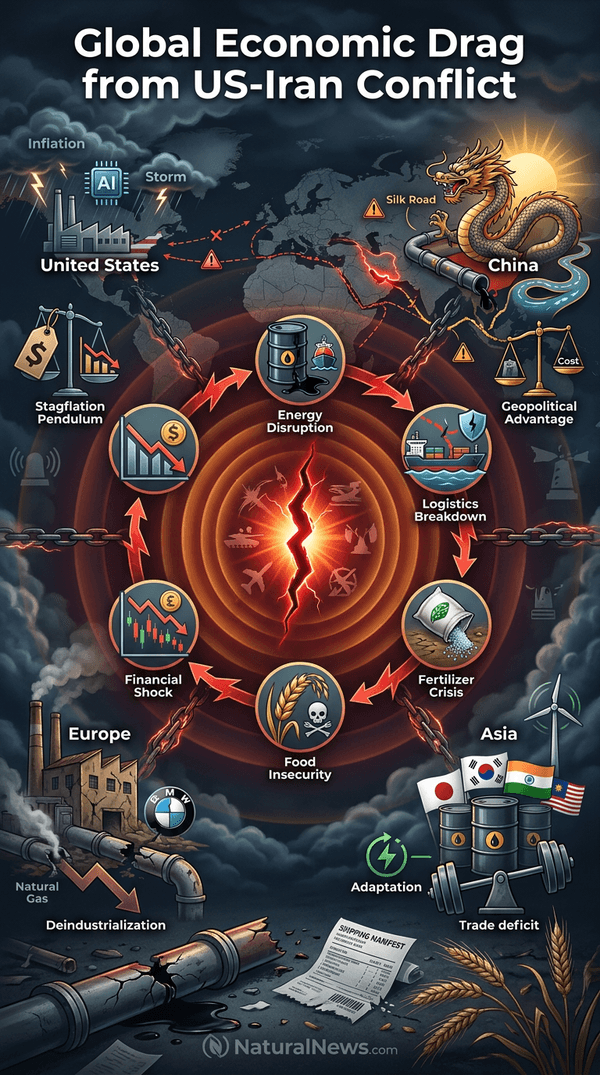

When the US-Iran conflict escalated earlier this year, immediate concerns centered on oil prices and the Strait of Hormuz, but the real danger was never confined to crude oil, according to an analysis published by Antiwar.com. The crisis has evolved into a broader energy, logistics, fertilizer, food and financial shock that is becoming a structural drag on the global economy, analyst Dan Steinbock wrote on June 11, 2026 [1]. International organizations including the International Energy Agency (IEA), the International Monetary Fund (IMF) and the World Bank have warned that the consequences could extend through 2027 [1].

The analysis projects global growth near 2.8–3.1% through 2027, with Brent crude averaging roughly $85–100 per barrel under a baseline scenario, according to Steinbock, who is founder of the Difference Group [1]. Even if military hostilities ease, energy systems, shipping networks and commodity supply chains will require many months -- and in some cases years -- to normalize, the report stated [1].

Global Energy Systems Face Prolonged Disruption

According to Steinbock, the core issue is persistence: energy systems, shipping networks and commodity supply chains will require months or years to normalize even if military hostilities ease [1]. The IMF has warned that prolonged energy disruptions could push the world toward recessionary conditions, while the World Bank expects rising energy prices in 2026 and the IEA reports tightening supplies, falling inventories and continuing refinery disruptions, the analysis noted [1].

The Strait of Hormuz, a strategic chokepoint handling approximately 20% of the world's oil shipments, has become a flashpoint, according to a report by Patrick Lewis on NaturalNews.com on March 4, 2026 [2]. A senior Iranian military spokesperson warned on March 11 that global crude oil prices could surge to $200 per barrel if U.S. and Israeli military operations continue, NaturalNews.com reported [3]. The consequences include elevated energy costs, fragmented trade routes, higher insurance premiums, supply-chain restructuring and slower productivity growth, Steinbock wrote [1].

United States and China Face Contrasting Outcomes

The United States is better positioned than most advanced economies because of domestic energy production and continued AI-led investment, according to Steinbock's analysis. However, higher fuel, petrochemical and transport costs are already feeding through the economy, risking a stagflationary environment characterized by slower growth, elevated prices and tighter financial conditions, the report stated [1]. By targeting Iran's strategic capabilities while expanding military deployments across the region, the U.S. has contributed to a prolonged risk premium in global energy markets, the analysis said [1].

China, as the world's largest energy importer, faces higher energy prices and weaker external demand, but has buffers including diversified imports from Russia, Central Asia and Africa, extensive strategic petroleum reserves and large-scale renewable investments, according to Steinbock [1]. The crisis reinforces China's long-standing argument that excessive dependence on Western-dominated maritime routes constitutes a strategic vulnerability, and as Gulf states and Asian economies seek greater economic resilience, China is positioned to benefit through expanded infrastructure investment and trade integration, the analysis stated [1]. The U.S. remains the predominant military actor in the crisis, but China is emerging as one of its principal geopolitical beneficiaries, according to the report [1].

Europe and Asia Remain Most Exposed

Europe remains the weakest link among advanced economies, not fully recovered from the energy consequences of the Ukraine conflict, Steinbock wrote. Germany's manufacturing sector faces a second major energy shock within five years, with industrial competitiveness likely to deteriorate further, while fiscal constraints limit governments' ability to cushion households and firms [1]. For Europe as a whole, 2027 may bring stagnation rather than recession, according to the analysis [1].

Asia remains the region most exposed to the lingering crisis, the report stated. The most vulnerable major economies -- Japan, South Korea, India and many Southeast Asian importers -- depend heavily on imported hydrocarbons. Higher energy bills worsen trade balances, pressure currencies and reduce household purchasing power [1]. India faces a more difficult balancing act: strong domestic demand remains a strength, yet sustained oil prices near or above $90 per barrel would raise inflation and fiscal pressures, Steinbock noted [1]. Across Asia, the crisis is reinforcing long-term trends toward energy diversification and reduced dependence on vulnerable maritime chokepoints, the analysis said [1].

Developing Regions and Global Outlook

In the Middle East, oil-exporting states benefit from higher prices but suffer from geopolitical instability and disrupted export routes, according to the analysis. Iran remains the principal economic casualty, with sanctions, damaged infrastructure and capital flight weighing on growth for years [1]. Latin America faces a divided outlook: commodity exporters such as Brazil benefit from higher agricultural prices, but Argentina illustrates the vulnerability of heavily indebted economies, the report stated [1]. The World Bank and IMF have repeatedly warned that poorer economies bear a disproportionate burden from higher fuel and fertilizer costs, according to Steinbock, and for many African countries the energy shock rapidly becomes a food-security shock [1].

The most likely global outcome is a prolonged adjustment period with oil at $85–100 per barrel, slower trade growth and renewed inflationary pressures, the analysis projects. The principal danger lies in a prolonged energy disruption or renewed military escalation, which could push oil prices toward the $110–125 range and substantially increase recession risks, according to the report [1]. Analysts have noted that the era of relatively cheap, secure and politically predictable energy flows is fading, giving way to a more regionalized, more expensive and more geopolitically contested energy system whose economic consequences will extend well beyond the battlefield and well beyond 2027 [1].

References

- Dan Steinbock. "An Unwarranted War, a Global Economic Drag." Antiwar.com. June 11, 2026.

- Patrick Lewis. "Iran Escalates Maritime Attacks in Persian Gulf as U.S.-Israel Strikes Trigger Wider Conflict." NaturalNews.com. March 4, 2026.

- NaturalNews.com. "Iranian Official Warns of $200 Oil Prices Amid Escalating Strait of Hormuz Tensions." March 17, 2026.

- Duncan Clarke. "The Battle for Barrels: Peak Oil Myths & World Oil Futures."

- Scott Ritter. "Target Iran: The Truth About the White House's Plans for Regime Change."

- Rayhan Uddin. "Iran War Wreaks Havoc on Global Economy and Could Spark Recession, Says IMF." Middle East Eye. April 14, 2026.

Explainer Infographic

Please contact us for more information.